Debt Consolidation Options: Simplify Your Financial Life

Are you struggling with multiple debts? Debt consolidation might be the answer.

It simplifies your finances by combining several debts into one payment. Managing various debts can be overwhelming. Different interest rates, due dates, and lenders can lead to missed payments and stress. Debt consolidation offers a way to regain control of your financial life. By merging your debts, you can reduce your interest rates and monthly payments. This can also improve your credit score over time. In this post, we will explore several debt consolidation options. Discover how you can streamline your finances and work towards a debt-free future. And if you are looking to boost your credit score, check out Boost Your Score for a structured credit-building program.

Introduction To Debt Consolidation

Struggling with multiple debts can be overwhelming. Debt consolidation offers a solution by combining all debts into one. This can make managing payments easier and less stressful. Let’s explore what debt consolidation is and its purpose.

Understanding Debt Consolidation

Debt consolidation involves taking out a new loan to pay off multiple debts. This new loan often has a lower interest rate. The goal is to reduce the overall cost of the debt.

There are different ways to consolidate debt:

- Personal loans

- Balance transfer credit cards

- Home equity loans

Each option has its pros and cons. Understanding them helps in making an informed decision.

The Purpose Of Debt Consolidation

The main purpose of debt consolidation is to simplify your finances. Instead of managing multiple payments, you only handle one. This can make budgeting easier.

Consolidating debt can also lead to lower monthly payments. This frees up cash for other expenses or savings. It can also help improve your credit score over time. Timely payments on the new loan can positively impact your credit history.

Remember, while debt consolidation can offer relief, it is not a cure-all. Good financial habits are essential for long-term success.

Key Features And Benefits Of Debt Consolidation

Debt consolidation can provide significant relief to individuals struggling with multiple debts. By combining all debts into one manageable payment, debt consolidation simplifies your financial life. Discover the key features and benefits that make debt consolidation a smart choice for many.

Simplified Payment Process

Managing multiple debts can be overwhelming. Debt consolidation allows you to merge all your debts into one single monthly payment. This process reduces the risk of missing payments and helps you stay organized. No more juggling multiple due dates and payment amounts.

Lower Interest Rates

One of the most appealing benefits of debt consolidation is the potential for lower interest rates. Many high-interest debts, such as credit cards, can be combined into a single loan with a lower rate. This reduction in interest can save you money over time and help you pay off your debt faster.

Improved Credit Score

Consolidating your debt can positively impact your credit score. By making consistent, on-time payments, you demonstrate financial responsibility. Over time, this can improve your credit score, making it easier to qualify for better financial products in the future.

Reduced Stress And Financial Anxiety

Debt can cause significant stress and anxiety. Consolidation offers a clear path to becoming debt-free, reducing the mental burden of managing multiple debts. Simplifying your payments and knowing you have a plan can provide peace of mind and improve your overall well-being.

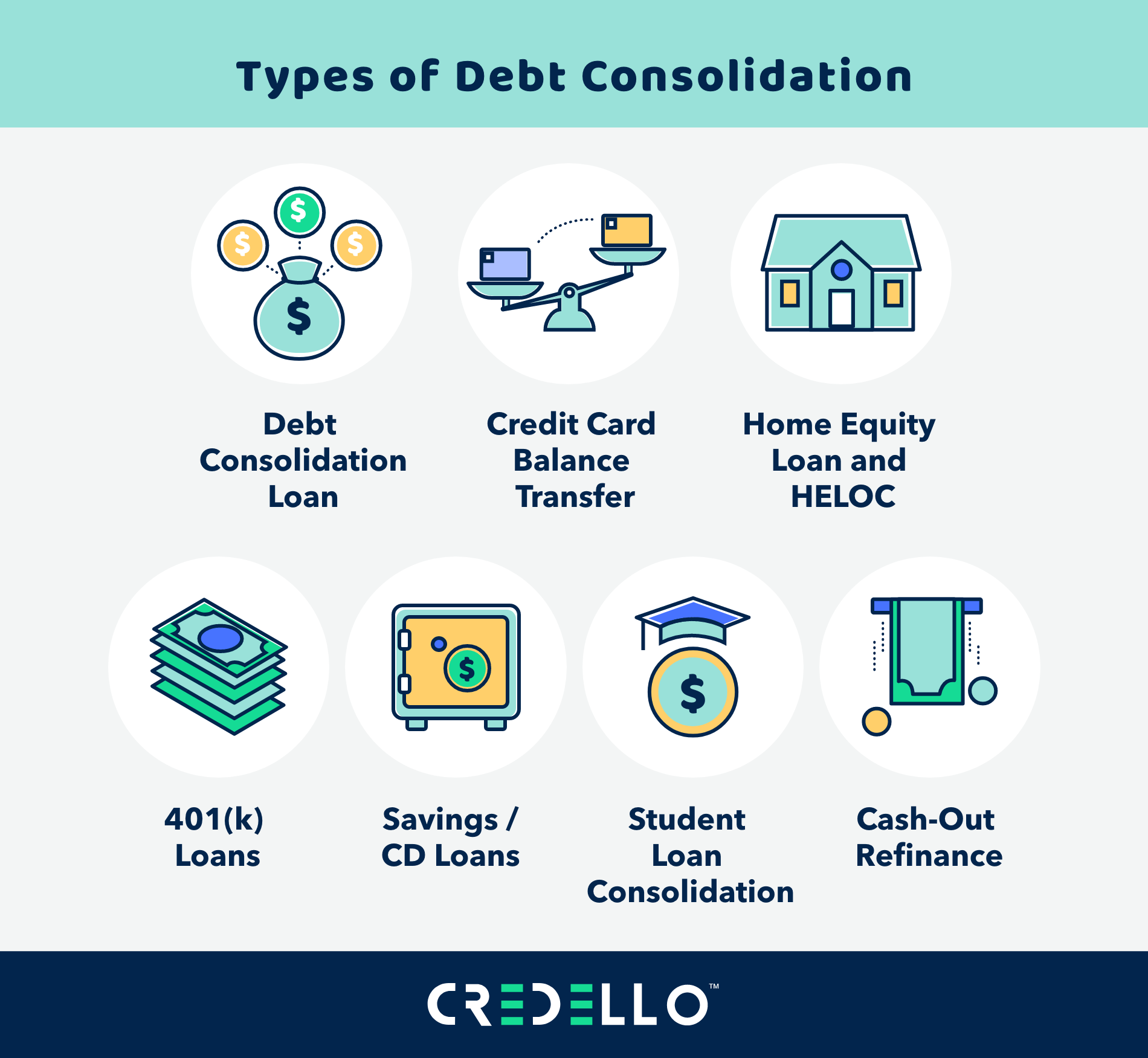

Types Of Debt Consolidation Options

Debt consolidation can simplify your financial life. It merges multiple debts into one, usually with a lower interest rate. Here, we explore the different types of debt consolidation options available.

Debt Consolidation Loans

Debt consolidation loans are personal loans used to pay off multiple debts. These loans typically offer a lower interest rate compared to credit cards. You then make a single monthly payment to the loan provider.

Balance Transfer Credit Cards

Balance transfer credit cards let you transfer high-interest debt to a card with a lower interest rate. Many balance transfer cards offer 0% APR for a promotional period, usually 12 to 18 months. This can save you money on interest if you pay off the balance within the promotional period.

Home Equity Loans

Home equity loans allow you to borrow against the equity in your home. These loans often have lower interest rates because they are secured by your home. However, if you fail to make payments, you risk losing your home.

Debt Management Plans

Debt management plans involve working with a credit counseling agency. The agency negotiates with your creditors to reduce interest rates and create a manageable payment plan. You make a single monthly payment to the agency, which then pays your creditors.

Debt Settlement

Debt settlement involves negotiating with creditors to settle your debt for less than what you owe. This option can significantly reduce your debt but may negatively impact your credit score.

For those looking to improve their credit score, consider using Boost Your Score. This program offers structured credit-building options that enhance credit scores through positive payment reporting and access to a secured credit card.

| Plan | Monthly Payment | Total Payment | Loan Amount | Est. APR | Est. Interest Rate |

|---|---|---|---|---|---|

| Mini Boost | $30/month | $360 | $300 | 34.82% | 35.56% |

| Boost | $64/month | $768 | $650 | 31.76% | 32.41% |

| Mega Boost (Best Value) | $82/month | $984 | $850 | 27.76% | 28.31% |

To learn more, contact Boost Your Score at 1 (800) 259-1270 or email at easy@boostyourscore.com.

Pricing And Affordability Of Debt Consolidation

Understanding the pricing and affordability of debt consolidation is essential. Different options come with varied costs, interest rates, and fees. Let’s dive into the specifics to help you make an informed decision.

Interest Rates And Fees

Interest rates and fees are major factors in determining the affordability of debt consolidation. Each option has its own structure:

- Personal Loans: Typically have fixed interest rates. You may face origination fees.

- Balance Transfer Credit Cards: Often offer 0% APR for an introductory period. Balance transfer fees may apply.

- Home Equity Loans: Usually have lower interest rates. However, you risk losing your home if you default.

Comparing these elements can help you find the most cost-effective solution for your situation.

Comparison Of Costs Across Different Options

Let’s compare the costs associated with different debt consolidation options:

| Option | Typical Interest Rate | Fees |

|---|---|---|

| Personal Loans | 5% – 36% | 1% – 6% origination fee |

| Balance Transfer Credit Cards | 0% APR for 12-21 months | 3% – 5% balance transfer fee |

| Home Equity Loans | 3% – 8% | Closing costs vary |

For instance, Boost Your Score offers three pricing plans:

- Mini Boost: $30/month for 12 months, totaling $360. Loan amount $300. Estimated APR 34.82%.

- Boost: $64/month for 12 months, totaling $768. Loan amount $650. Estimated APR 31.76%.

- Mega Boost: $82/month for 12 months, totaling $984. Loan amount $850. Estimated APR 27.76%.

Understanding the cost structure and comparing these details can guide you in selecting the best debt consolidation option for your needs.

Pros And Cons Of Debt Consolidation

Debt consolidation is a financial strategy that combines multiple debts into a single payment. It aims to simplify debt management and reduce interest rates. This section covers the pros and cons of debt consolidation to help you decide if it’s the right choice for you.

Advantages Of Debt Consolidation

Debt consolidation offers several benefits that can make managing your finances easier.

- Single Monthly Payment: Combining multiple debts into one reduces the stress of handling several payments.

- Lower Interest Rates: Consolidation loans often come with lower interest rates than credit cards.

- Improved Credit Score: Consistently making payments on time can improve your credit score.

- Predictable Payments: Fixed monthly payments make budgeting easier.

Potential Drawbacks And Risks

While debt consolidation has its advantages, it also comes with potential risks that you should consider.

- Fees and Costs: Some consolidation loans come with fees that can add to your debt.

- Longer Repayment Period: Extending the loan term can result in paying more interest over time.

- Risk of Falling Into Debt Again: Without proper financial discipline, you may accumulate new debts.

- Impact on Credit Score: Initially, applying for a consolidation loan might slightly lower your credit score.

Understanding the pros and cons of debt consolidation can help you make an informed decision. If you need help improving your credit score, consider a structured program like Boost Your Score. This program offers a secured credit card and positive credit history reporting to help you build a better financial future.

:max_bytes(150000):strip_icc()/debtconsolidation.asp-final-18e80676e0af4379a7962bfc4a0874de.png)

Specific Recommendations For Ideal Users

Debt consolidation can be a valuable tool for managing and reducing debt. However, it is essential to understand when it is the right option for you. Below, we provide specific recommendations to help you determine if debt consolidation is suitable for your financial situation.

When Debt Consolidation Is Right For You

Debt consolidation may be an ideal solution if you:

- Have multiple debts with high-interest rates.

- Struggle to manage various debt payments each month.

- Have a steady income and a good credit score.

- Want to simplify your finances by combining your debts into one payment.

- Seek to lower the overall interest rate on your debts.

Using a structured credit-building program like Boost Your Score can also enhance your financial health. This program helps you build a positive payment history, which is crucial for debt consolidation.

Scenarios Where Debt Consolidation May Not Be The Best Option

Debt consolidation might not be the best choice if:

- You have a low credit score, making it difficult to secure favorable terms.

- Your income is unstable or insufficient to manage a new consolidated payment.

- You have a small amount of debt that can be managed with other methods.

- You are not committed to changing your spending habits, which could lead to accumulating more debt.

- You do not fully understand the terms and conditions of the consolidation loan.

In such cases, focusing on budgeting and using tools like Boost Your Score to improve your credit rating might be more effective.

Here’s a comparison of the Boost Your Score plans to consider:

| Plan | Monthly Payment | Total Payment | Loan Amount | Estimated APR | Estimated Interest Rate |

|---|---|---|---|---|---|

| Mini Boost | $30/month | $360 | $300 | 34.82% | 35.56% |

| Boost | $64/month | $768 | $650 | 31.76% | 32.41% |

| Mega Boost | $82/month | $984 | $850 | 27.76% | 28.31% |

By understanding these scenarios and utilizing programs like Boost Your Score, you can make informed decisions about your debt management strategy.

Frequently Asked Questions

What Is Debt Consolidation?

Debt consolidation involves combining multiple debts into one single loan. This simplifies monthly payments and can reduce interest rates.

How Does Debt Consolidation Work?

Debt consolidation works by taking out a new loan to pay off existing debts. This leaves you with one monthly payment.

Are There Different Types Of Debt Consolidation?

Yes, there are different types. They include personal loans, balance transfer credit cards, and home equity loans.

Can Debt Consolidation Lower My Interest Rate?

Yes, debt consolidation can lower your interest rate. This can save you money over time and simplify payments.

Conclusion

Debt consolidation can simplify managing multiple debts. Evaluate your options carefully. Choose a plan that suits your financial situation. Remember, improving your credit score is essential. Consider using Boost Your Score. It offers structured credit-building programs. Positive payment history can enhance your creditworthiness. Stay committed to your financial goals. Consistent efforts will lead to better credit health. Always seek professional advice when needed.