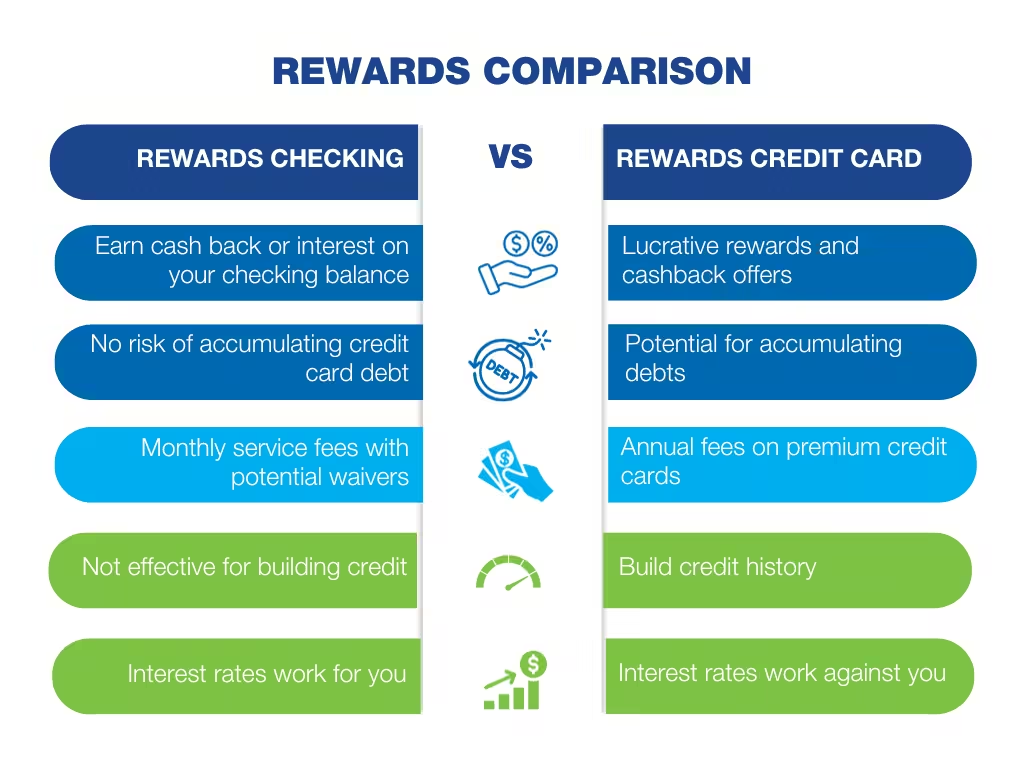

Rewards Vs. Cashback Credit Cards: Maximize Your Benefits

Choosing between rewards and cashback credit cards can be tough. Both offer unique benefits.

Rewards credit cards provide points or miles for every dollar spent, while cashback cards give a percentage of your spending back as cash. Understanding the differences between rewards and cashback credit cards helps you pick the best option. Rewards cards often come with travel perks, but they may have higher annual fees. Cashback cards are straightforward, offering simple cash returns on purchases. Deciding which card suits your lifestyle can maximize your financial benefits. For instance, the Possible Card offers a unique solution with no interest and helps build credit history. Whether you prefer rewards or cashback, knowing the pros and cons will help you make an informed choice. Learn more about the Possible Card and its features here.

Introduction To Rewards And Cashback Credit Cards

Choosing the right credit card can be challenging with numerous options available. Rewards and cashback credit cards are two popular types that offer distinct advantages. Knowing the difference can help you make an informed decision.

Understanding Rewards Credit Cards

Rewards credit cards offer points, miles, or other incentives for every dollar spent. These points can be redeemed for various benefits such as travel, merchandise, or gift cards. Rewards are usually tiered, meaning certain purchases may earn more points than others.

For example, some cards offer higher points for travel-related expenses, while others focus on dining or grocery purchases. The value of these rewards varies, so it is essential to understand the redemption options and their worth.

Understanding Cashback Credit Cards

Cashback credit cards provide a straightforward benefit: a percentage of your spending is returned to you as cash. This cash can be redeemed as statement credits, direct deposits, or even checks. Cashback percentages can vary based on the spending category.

Some cards offer a flat rate for all purchases, while others have higher rates for specific categories like gas or dining. Cashback cards are ideal for those who prefer simplicity and immediate rewards.

Purpose Of The Article

The goal of this article is to help you understand the differences between rewards and cashback credit cards. By the end, you will have the knowledge to choose the card that best suits your spending habits and financial goals.

Whether you aim to earn travel points or prefer cash in hand, understanding these options will guide you in making a smart financial decision.

For those with a challenging credit history, considering products like the Possible Card from Possible Finance can be beneficial. This card offers a credit limit without a credit check, along with features like no interest and no late fees, helping to build your credit history.

Key Features Of Rewards Credit Cards

Rewards credit cards offer various benefits that can enhance your financial experience. They provide opportunities to earn points, miles, or cashback on everyday purchases. Understanding the key features of these cards can help you maximize their advantages.

Types Of Rewards Programs

There are several types of rewards programs available:

- Points Programs: Earn points for every dollar spent. Points can be redeemed for various rewards.

- Miles Programs: Ideal for frequent travelers. Earn miles on purchases and redeem them for flights and travel-related expenses.

- Cashback Programs: Earn a percentage of your spending back as cash. This is usually credited to your account or given as a statement credit.

How Points And Miles Work

Points and miles accumulate based on your spending. The earning rate varies by card:

- Possible Card: Unlock a $400 or $800 credit limit instantly¹ with no interest.

- Possible Loan: Borrow up to $500 instantly^ with no late or penalty fees.

Typically, 1 point or mile is earned per dollar spent. Some cards offer bonus points for specific categories like dining or travel.

Redemption Options And Flexibility

Rewards credit cards offer flexible redemption options:

- Travel: Use points or miles for flights, hotel stays, and car rentals.

- Gift Cards: Redeem points for gift cards from various retailers.

- Cashback: Convert points into cash or statement credits.

Each card has its own redemption process, making it important to choose one that aligns with your spending habits.

Exclusive Perks And Bonuses

Rewards credit cards often come with exclusive perks and bonuses:

- Sign-Up Bonuses: Earn extra points or miles after meeting initial spending requirements.

- Travel Benefits: Access to airport lounges, travel insurance, and priority boarding.

- Purchase Protection: Extended warranties and purchase protection on items bought with the card.

These perks can add significant value, making your card more rewarding.

Key Features Of Cashback Credit Cards

Cashback credit cards offer a simple and rewarding way to save money on everyday purchases. They return a percentage of your spending as cash, either as a flat rate or a tiered rate. Here, we explore the key features of cashback credit cards, helping you understand their benefits and how to maximize your rewards.

Flat-rate Vs. Tiered Cashback

Cashback credit cards come in two main types: flat-rate and tiered cashback.

- Flat-rate cashback cards offer a consistent percentage on all purchases. For example, you might earn 1.5% back on every dollar spent.

- Tiered cashback cards provide higher percentages on certain categories. You could earn 3% on groceries, 2% on gas, and 1% on all other purchases.

Cashback On Everyday Purchases

Many cashback cards focus on everyday spending categories to maximize your savings.

Examples include:

- Groceries: Earn up to 3% cashback on grocery store purchases.

- Gas: Get 2% cashback at gas stations.

- Dining: Receive 1% to 2% cashback at restaurants.

- Online Shopping: Some cards offer special rates for online purchases.

Cashback Redemption Options

Cashback redemption can be straightforward or offer various choices.

| Redemption Option | Description |

|---|---|

| Statement Credits | Apply cashback directly to your credit card balance. |

| Bank Deposits | Transfer cashback to your bank account. |

| Gift Cards | Exchange cashback for gift cards from various retailers. |

| Charity Donations | Donate your cashback to a charity of your choice. |

Additional Card Benefits

Many cashback cards offer more than just cashback rewards.

Additional benefits may include:

- No Annual Fees: Many cashback cards do not charge an annual fee.

- Introductory Bonuses: Earn a bonus after spending a certain amount in the first few months.

- Travel Perks: Some cards offer travel-related benefits like rental car insurance or no foreign transaction fees.

- Purchase Protection: Protection for new purchases against damage or theft.

Pricing And Affordability

When choosing between rewards and cashback credit cards, understanding the pricing and affordability is crucial. This section will cover key aspects such as annual fees, interest rates, foreign transaction fees, and balance transfer fees. We will also compare the costs between different card types to help you make an informed decision.

Annual Fees And Interest Rates

Rewards credit cards often come with an annual fee, which can range from $50 to $550 or more. These fees are typically justified by the benefits and rewards offered. Cashback cards might also have annual fees, but they tend to be lower, ranging from $0 to $100.

Interest rates are another important factor. Rewards cards usually have higher APRs, averaging around 16% to 25%. Cashback cards, on the other hand, might have slightly lower APRs, typically between 13% and 23%. Choosing a card with a lower APR can save you money if you carry a balance.

Foreign Transaction Fees

Many credit cards charge foreign transaction fees, typically around 1% to 3% of each purchase made abroad. This fee can add up quickly if you travel frequently. Some rewards cards, especially travel-focused ones, waive these fees entirely. Cashback cards might still charge foreign transaction fees, so it’s essential to check the card’s terms.

Balance Transfer Fees

If you plan to transfer a balance from one card to another, balance transfer fees are a significant consideration. These fees usually range from 3% to 5% of the transferred amount. Both rewards and cashback cards may offer promotional balance transfer rates, but it’s important to read the fine print. A lower balance transfer fee can help you save money when consolidating debt.

Comparing Costs Between Card Types

| Card Type | Annual Fee | Interest Rate (APR) | Foreign Transaction Fee | Balance Transfer Fee |

|---|---|---|---|---|

| Rewards Card | $50 – $550+ | 16% – 25% | 1% – 3% (Some cards waive this fee) | 3% – 5% |

| Cashback Card | $0 – $100 | 13% – 23% | 1% – 3% | 3% – 5% |

In summary, both rewards and cashback credit cards come with various costs. Rewards cards often have higher annual fees and interest rates, but they can offer significant benefits. Cashback cards are usually more affordable with lower fees, making them a good option for budget-conscious users.

Pros And Cons Of Rewards Credit Cards

Rewards credit cards offer incentives such as points, miles, or cash back for every dollar spent. These cards can be very appealing, but they come with both advantages and disadvantages. Understanding these pros and cons can help you make an informed decision about whether a rewards credit card is the right choice for you.

Advantages Of Rewards Programs

- Earn Points or Miles: Many rewards cards let you earn points or miles for every purchase. These can be redeemed for travel, gift cards, or merchandise.

- Cashback Offers: Some rewards cards offer cashback on purchases. You can use this cashback to offset your balance or save for future expenses.

- Sign-up Bonuses: Many rewards cards come with attractive sign-up bonuses. Spend a certain amount within the first few months and get bonus points or miles.

- Exclusive Perks: Rewards cards often offer exclusive perks like access to airport lounges, special event tickets, or travel insurance.

Drawbacks To Consider

- Higher Interest Rates: Rewards cards often come with higher interest rates. This can be costly if you carry a balance.

- Annual Fees: Many rewards cards have annual fees. These fees can range from $50 to several hundred dollars.

- Complex Redemption Rules: The process for redeeming rewards can be complicated. Some programs have blackout dates or limit how you can use your points or miles.

- Temptation to Overspend: The allure of earning rewards can lead to overspending. This can result in debt and negate the benefits of the rewards.

Ideal Users For Rewards Cards

Rewards credit cards are best suited for individuals who:

- Pay off their balance in full each month.

- Have good to excellent credit scores.

- Travel frequently or make large purchases regularly.

- Can maximize the value of the rewards and perks offered.

For those who prefer a simpler option or have lower credit scores, the Possible Card from Possible Finance could be a great alternative. The Possible Card offers a $400 or $800 credit limit instantly with no credit check, 0% interest forever, and no late fees. This card is designed to help users build credit history and manage finances without the burden of high fees or interest.

Pros And Cons Of Cashback Credit Cards

Cashback credit cards offer a straightforward way to earn money back on everyday purchases. Understanding their benefits and drawbacks can help you decide if they are the right choice for your financial needs.

Benefits Of Cashback Offers

Cashback credit cards can provide real savings on purchases. Here are some key advantages:

- Simple Rewards: Earn a percentage of your spending back as cash. This is often easier to understand than points-based systems.

- Versatility: Use cashback for anything, including paying down card balances.

- Immediate Rewards: Most cashback cards do not require you to accumulate points before redeeming.

These benefits make cashback cards appealing to many users.

Potential Downsides

While cashback cards have many perks, they also come with potential downsides:

- Annual Fees: Some cards charge annual fees that might offset your rewards.

- Interest Rates: High-interest rates can negate cashback benefits if you carry a balance.

- Reward Caps: Some cards limit the amount of cashback you can earn in a year.

These factors are important to consider when choosing a cashback card.

Ideal Users For Cashback Cards

Cashback cards work best for certain types of users:

- Regular Spenders: Those who use their credit cards frequently for everyday purchases.

- Responsible Borrowers: Individuals who pay off their balances monthly to avoid interest charges.

- Seekers of Simplicity: Users who prefer straightforward rewards without the hassle of managing points.

If you fit into these categories, a cashback credit card might be a great fit for you.

Making The Choice: Rewards Vs. Cashback

Choosing between rewards and cashback credit cards can be challenging. Both offer unique benefits that cater to different needs. Understanding how each type works will help you make the right decision.

Assessing Your Spending Habits

Review your monthly expenses. Identify where you spend the most. If you spend a lot on groceries and gas, a rewards card may offer more value. Cashback cards are ideal for those who want simple cash returns on all purchases.

- High Spending Categories: Travel, dining, groceries

- General Spending: Everyday purchases, bills

Evaluating Your Financial Goals

Consider your financial objectives. Do you want to save money or earn travel points? Cashback cards are straightforward, providing immediate returns. Rewards cards offer points or miles that can be redeemed for travel, merchandise, or gift cards.

- Immediate Savings: Cashback cards

- Future Benefits: Rewards cards

Matching Card Features To Your Lifestyle

Align card features with your lifestyle. For instance, the Possible Card offers a $400 or $800 credit limit without a credit check. It is ideal for those who need accessible credit without interest or late fees.

| Feature | Possible Card | Typical Rewards Card |

|---|---|---|

| Credit Limit | $400 or $800 | Varies |

| Interest Rate | 0% | Variable |

| Late Fees | None | Yes |

| Monthly Fee | $8 or $16 | None or Annual Fee |

When To Switch Between Card Types

Switching card types can be beneficial. If your spending patterns change, consider switching. For instance, if you start traveling more, a rewards card might offer better benefits.

- Change in Spending Habits: New spending categories

- Financial Goals Shift: Different savings or rewards objectives

Making an informed choice between rewards and cashback cards involves understanding your spending habits, financial goals, and aligning card features with your lifestyle. The Possible Card offers a unique solution for those seeking accessible credit without the burden of interest or late fees.

Specific Recommendations For Different Users

Choosing between rewards and cashback credit cards depends on your spending habits and financial goals. Below, we offer tailored recommendations for different types of users. Each category is designed to help you select the most suitable card for your needs.

Frequent Travelers

If you travel often, a rewards credit card can be highly beneficial. Look for cards that offer:

- Airline miles

- Hotel points

- Travel insurance

- No foreign transaction fees

For instance, the Possible Card provides a $400 or $800 credit limit instantly with no interest, making it a great option for travelers who want to avoid high fees. The monthly fee is $8 or $16, which is affordable for frequent travelers.

Everyday Spenders

If your spending is mostly on daily necessities like groceries and fuel, a cashback card may suit you better. Look for cards offering:

- High cashback rates on groceries and fuel

- No annual fees

- Introductory cashback bonuses

The Possible Card offers 0% interest forever, no late fees, and helps build credit history, which is ideal for everyday spenders.

Business Owners

Business owners should seek cards that offer rewards for business-related expenses. Consider cards that provide:

- Cashback or rewards on office supplies and travel

- Expense tracking tools

- Employee cards

The Possible Loan allows you to borrow up to $500 instantly with no late or penalty fees, making it a viable option for managing business expenses.

Students And Young Professionals

Students and young professionals often need a credit card that helps build credit while offering some rewards. Look for cards with:

- No credit check

- Low or no annual fees

- Rewards for everyday purchases

The Possible Card is perfect for this group as it requires no credit check, charges a monthly fee of $8 or $16, and has no late fees. It also helps in building credit history, which is crucial for young adults.

Conclusion: Maximizing Your Benefits

Choosing between rewards and cashback credit cards can be tricky. Each type offers unique advantages. To get the most out of your card, consider your spending habits and financial goals.

Summarizing Key Points

Understanding the differences between rewards and cashback credit cards is essential. Rewards cards often offer points or miles, ideal for travelers or frequent shoppers. Cashback cards provide a percentage back on purchases, which is straightforward and easy to use.

Here is a quick comparison:

| Type | Benefits | Best For |

|---|---|---|

| Rewards Cards | Points/Miles, Travel perks | Frequent Travelers, Shoppers |

| Cashback Cards | Cashback, Simple redemption | Everyday Spending |

Final Tips For Cardholders

- Assess your spending habits.

- Check card fees and interest rates.

- Ensure the card aligns with your financial goals.

- Pay off your balance monthly to avoid interest charges.

- Monitor your credit score to benefit from potential upgrades.

For those with less-than-perfect credit, products like the Possible Card from Possible Finance might be beneficial. This card helps build credit, has no late fees, and charges 0% interest.

Resources For Further Reading

For more information on choosing the right credit card, check out these resources:

Making an informed choice can help you maximize your benefits and achieve your financial goals.

:max_bytes(150000):strip_icc()/cash-back.asp-final-e756ec89261f4a61967131694a008c33.png)

Frequently Asked Questions

What Are Rewards Credit Cards?

Rewards credit cards offer points or miles for purchases. These points can be redeemed for travel, merchandise, or cash.

How Do Cashback Credit Cards Work?

Cashback credit cards give a percentage of the purchase amount back as cash. This cash can be used for statement credits or deposited into your account.

Which Is Better, Rewards Or Cashback Cards?

It depends on your spending habits and goals. Rewards cards are great for travel enthusiasts, while cashback cards offer straightforward savings.

Do Rewards Cards Have Annual Fees?

Many rewards cards have annual fees, but they often offer higher rewards. Always check the card’s benefits before applying.

Conclusion

Choosing between rewards and cashback credit cards depends on your spending habits. Rewards cards offer points for travel, dining, and more. Cashback cards provide direct cash savings on purchases. Both have their unique benefits. Evaluate your financial goals and preferences. For those seeking accessible credit, consider the Possible Card and Possible Loan by Possible Finance. They offer fair terms and no hidden fees, making them a solid choice for building credit. Make an informed decision to maximize your financial benefits.